Victoria's debt is nearly $200 billion. Is that really so bad?

The mechanics of this debt - explained.

With the release of each state budget, the conversation about Victoria’s debt becomes louder and more frightening.

However, the mechanics of this debt are rarely explained.

What is debt?

Monash University associate professor of economics Jaai Parasnis defines debt as the amount you borrow when you spend more than the revenue you generate.

Government debt is no different.

What distinguishes it from the debt an everyday person may accrue is that the dollar figures lose meaning without context.

“Generally, we tend to look at [government debt] as a proportion of gross domestic product (GDP),” Dr Parasnis said.

“And as long as the economy is growing, the GDP is growing," she said.

“So even though the dollar figure of the debt is high as a proportion of your whole economy, it will become smaller and maybe not much to worry about.”

Building on this, David Richardson, a senior research fellow in economics at The Australia Institute, said debt is neither inherently good nor bad.

“There are a lot of people who talk about debt as some evil thing that we should get rid of,” Richardson said.

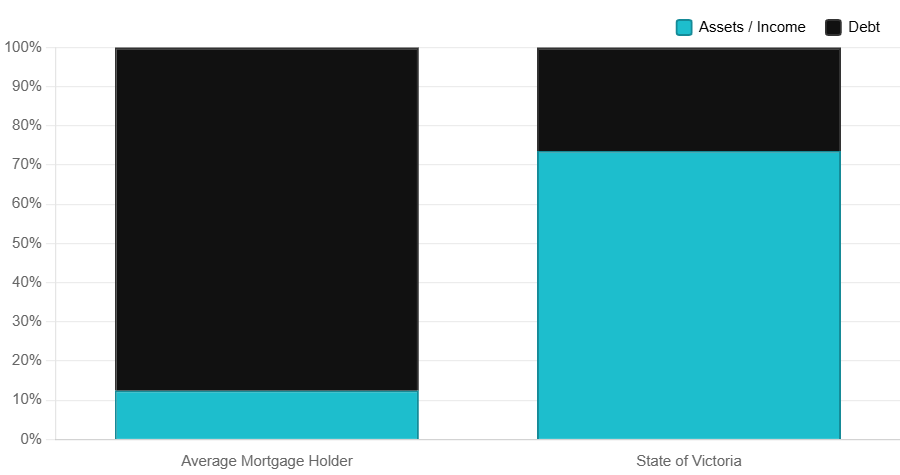

“But the private sector doesn't think it's a good idea to pay off debt. About 8 million households in Australia happily have a house with a mortgage," he said.

“The average mortgage at the moment is a little bit over $700,000, and earnings are around $100,000, so people happily have mortgages around seven times average yearly earnings.”

According to the Victorian State Treasury, Victoria’s GDP sits at $637 billion.

Victoria's debt as of the 2026-27 financial year will be $165.3 billion, or 25 per cent of GDP, compared to $460 billion in assets.

In 2030, Victoria’s debt is set to rise to $200 billion while its assets will increase to $520 billion.

“So despite debt growing, the state's net worth is growing even more rapidly,” Richardson said.

Where did it come from?

Victoria's current debt load reflects a decade of heavy infrastructure investment, including the $90 billion Big Build transport program alongside significant public health expenditure during COVID-19.

The government financed these projects by issuing bonds.

When the government issues bonds, it means anyone with excess savings can lend money to the state to build an asset.

In return, the investor will receive interest on their low-risk investment, which the government will pay off overtime.

“As an investor, you do look at whether the government has some credible plan to pay you back or not,” Dr Parasnis said.

“If the government is borrowing too much, [investors] become worried about the riskiness of that borrowing, and [will ask for] a higher return to lend money.”

She said debt may become a problem when it is too high a proportion of income, making borrowing more expensive, or when it comes from sources that do not maximise future revenue or the public good.

“Theoretically, if you are spending on something that will finance education, that is less of a worry, even though the debt might be high,” she said.

“But if you take a debt and go on a holiday, then that is more of a worry," she said.

“The same thing is true with the government debt: what is that being used for?”

She said the government can and should justify spending beyond current means to invest in better well-being and higher future earning capacity.

Richardson made a similar point using a corporate lens.

“If you looked at BHP’s books and found they're investing more than their profits, you wouldn't care, so long as they're making a profit covering any current expenses,” he said.

Governments, he argued, should be assessed by the same logic.

“What's the point of not going into debt? It means you can only invest up to the money that you actually receive, and why would you limit yourself to that?”

When do you pay it off?

Dr Parasnis said the repayment timeline depends on what the debt was used for and whether it strains the state's capacity to borrow again.

Even productive investment in education, healthcare and infrastructure can still strain the state's borrowing capacity.

“You really want to, during the good years, have low debt, pay off previous debt, so that when the bad years come, you have the capacity to go out and spend," Dr Parasnis said.

“We were lucky as a country that when the global financial crisis hit, or the COVID situation happened, our finances were quite strong, and our debt wasn't too high.”

Because Victoria had only $25 billion of debt in 2019, totalling just 5.5 per cent of the state's GDP, investors were willing to lend money at a lower rate and trusted it would be repaid when COVID hit.

Dr Parasnis said the more important question is not the total amount of debt, but what the money was spent on and how it will be serviced.

“I don't think the money is really being spent in the best value proposition, so that is the main worry for me, rather than the total amount,” she said.

How do you pay it off?

Governments have far more flexibility than individuals when it comes to managing debt.

They own public assets that can be sold, and they have the sovereign power to raise revenue through taxation.

“A household cannot stretch itself too much, but the government could, because it always has the sovereign power to tax you,” Dr Parasnis said.

Additionally, the government endures in perpetuity, unlike a person who works for 40 years, meaning the debts can be paid over multiple generations.

“Whatever we are building now, the actual fruits of that will be enjoyed by the next generation,” she said.

“So if we have to pay the interest on that by borrowing, the future generations are going to have better options, [especially] if that grows the economy, they are going to have better capacity to pay it off.”

But Richardson cautioned that political pressure to pay down debt aggressively carries real costs.

Reducing government debt by $20 billion per year, for instance, requires either cutting spending by that amount or raising equivalent revenue, and cutting spending reduces the capacity of ordinary people to participate in the economy.

He pointed to the United Kingdom under Margaret Thatcher as a cautionary example.

Thatcher reduced government debt by slashing public services and tolerating high unemployment.

“Julius Caesar created a desert and called it stability; this is basically what Thatcher did by increasing unemployment and flattening economic activity, and calling that stability," he said.

“The functional finance view is that the government should accept the responsibility of achieving full employment with low inflation, and whatever is needed to achieve those objectives is what you recommend.”

Victoria's $165 billion debt sits alongside $460 billion in assets and a growing economy. The real questions are whether the investment was well directed, whether borrowing capacity remains intact for the next crisis, and whether future Victorians will judge it worthwhile.